What is factor investing: The essentials

Factor investing is about investing in securities featuring certain characteristics that have proved to deliver higher risk-adjusted returns than the market over time, following a fixed set of rules. In other words, it is based on the systematic exploitation of a number of premiums, called factor premiums, that have shown to be robust over time and across different markets.

An example of this is the value factor: securities that are attractively priced relative to their fundamental value, for example stocks exhibiting a low book-to-price ratio (which compares a company’s market value to its book value), tend to outperform in the long run.

Factor premiums have been extensively documented in academic literature for over four decades. Although they were initially discovered in the stock market, these premiums can also be found in most asset classes, including bonds, currencies and commodities. In fact, factor investing can be applied both within and across multiple asset classes.

A history going back four decades

The origins of factor investing date back to the 1970s, when empirical studies started challenging the prevailing assumptions of the Capital Asset Pricing Model (CAPM) and the Efficient Market Hypothesis (EMH) for equities. These financial theories assume that markets are efficient, that investors are rational and that more risk leads to higher returns.

According to the EMH, it’s impossible to consistently beat the market because all participants are rational and always have access to all relevant information, to which they react instantaneously. As a result, securities always trade at their fair value, making it impossible for investors to either buy undervalued securities or sell them at inflated prices. In practice, of course, market participants don’t all receive or react to information simultaneously, and they don’t always act rationally.

Although the empirical foundations of factor investing were laid over 40 years ago, its real breakthrough came in 2009 with the publication of the Evaluation of Active Management of the Norwegian Government Pension Fund – Global report.2 This groundbreaking paper analysed the performance of one of the world’s largest sovereign wealth funds after it suffered heavy losses as the global financial crisis deepened in 2008.

Authored by three finance professors—Andrew Ang, William Goetzmann and Stephen Schaefer—the report showed that the performance of the fund’s active managers did not actually reflect their true skill. Rather, it could in large be explained by the fund’s implicit exposure to a number of factors. Based on their findings, they recommended a long-term strategy incorporating an explicit top-down exposure to proven factors to maximise returns.

Factor investing today

In the ensuing years, prominent institutional investors have publicly embraced more systematic approaches to portfolio allocation and security selection based on these insights. Factor investing has rapidly gained popularity among professional investors around the world. Asset managers and market index providers have also dived in and increased the breadth of their offering in this field.

Estimates of the amount of money invested in factor strategies vary from one source to another, ranging from USD 1 to 2 trillion globally in most cases. In a report published in October 2017, Morgan Stanley estimated that almost USD 1.5 trillion was invested in smart beta, quant and factor-based strategies and that assets under management have been growing by 17 per cent per year on average since 2010.

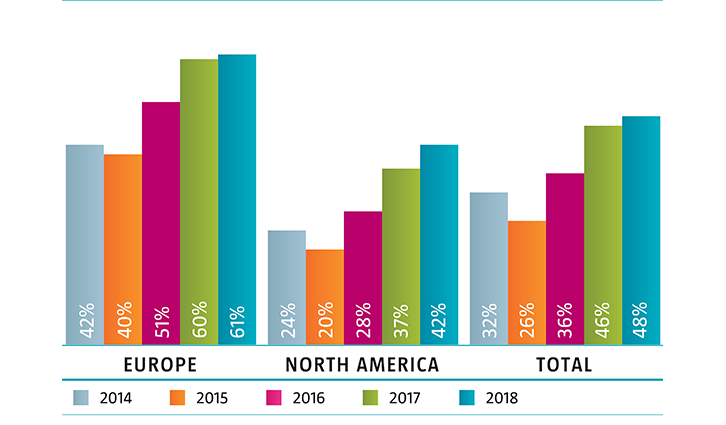

Smart beta adoption percentage by region

Source: FTSE Russell, Smart beta: 2018 global survey findings from asset owners

According to a 2018 survey by asset manager Invesco, factor allocations accounted for approximately 16 per cent of total portfolio allocations of institutional asset owners having adopted factor investing. According to another survey by FTSE Russell, 48 per cent of asset owners worldwide have implemented smart beta, in other words factor-based strategies, in their portfolios in 2018.5

To sum up, factor investing emerged from the first empirical tests of the CAPM in equity markets, in the 1970s, to become a widespread investment approach nowadays.

Three key concepts

The definitions of concepts such as quantitative investing, factor investing, or smart beta are far from set in stone. Indeed, views on what these terms mean can vary significantly from one asset manager to another, and from one investor to another.

Quant investing:

Quant investing can be defined as the use of quantitative data analysis and rules-based securities selection models to build portfolios in a systematic way. Contrary to fundamental investing, where the portfolio manager remains the sole decision maker, quant strategies use a model as the main driver of security selection.

Factor investing:

Factor investing is a form of quant investing that is based on the exploitation of academically-proven factor premiums. This can be implemented within and across many different asset classes. Factors represent certain security-specific attributes that explain the return and risk of a group of securities in the long run.

Smart beta:

Smart beta strategies explicitly target factor premiums and represent an alternative to traditional market capitalisation-weighted indices (beta). The term smart beta could, in theory, be used to describe any kind of factor-based strategy. However, it is often associated with generic factor strategies—typically marketed through exchange-traded funds (ETFs)—based on publicly available ‘smart beta’ indices.