The overwhelming majority of superannuation fund members fall into their fund’s default option. Consequently, at the point of retirement many are faced, for the first time, with the need to make a choice for their investment option. Clearly investment risk is a major if not the major consideration in making their choice.

At a Sydney conference last year, a highly-credentialed panel of investment risk measurement experts from the UK, the USA and Australia were asked the question “is volatility an appropriate measure of risk for a superannuation fund?” Each of the three panel members responded “no”. This is of concern given that volatility is and has been consistently used as a proxy for risk by the superannuation industry.

The key to the solution lies in (a) defining ‘risk’ in the context of a superannuation fund member, particularly when entering draw down phase and (b) recognising that risk and return cannot be viewed independently. The two are inextricably linked and a meaningful measure of risk must also consider any associated risk/return trade-off.

Traditional measures of risk

The shortcoming of traditional risk measures is that risk is not fully defined in the context of a superannuation fund member. Traditional ‘risk measures’ are in fact all measures of short term volatility.

For a member of a superannuation fund, their risk is far better defined as ‘the probability of running out of money during retirement’. This may have little or no correlation with short term market volatility.

It would be fair to say that the risk measures defined on MySuper dashboards have been the subject of some debate and indeed criticism over recent times.

Why has the superannuation industry adopted the risk measure it so commonly uses?

Market volatility is easy to measure and the investment industry has universally embraced volatility as a proxy for risk over decades. Perhaps surprisingly, this appears to have been done without appropriately defining risk in the context of the asset owner’s objectives.

Arguably, investment managers tend to be focused on short term investment horizons (consistent with their incentive bonuses) and have not been consistently incentivised to think in the context of an investment horizon exceeding half a century within which superannuation fund members operate.

While market volatility may be a useful proxy for risk over the short-term periods of a few months or even a few years, it is not useful for the long-term investment horizons (60-70 years) of superannuation fund members.

The following two charts illustrate the difference between market volatility and ‘the risk of running out of money in retirement’.

Relative Fiscal Year Returns (%)

Source: Vanguard Investments Australia, Athena IOC

The chart above shows the annual fiscal year returns over the 46-year period between 1971 and 2016. Cash consistently returns between +1 per cent and +19 per cent. Australian equities produce a far wider range of returns between -25 per cent and +78 per cent. By any of the risk measures traditionally adopted by the superannuation industry, Australian equities appear to be a far ‘riskier’ option than cash.

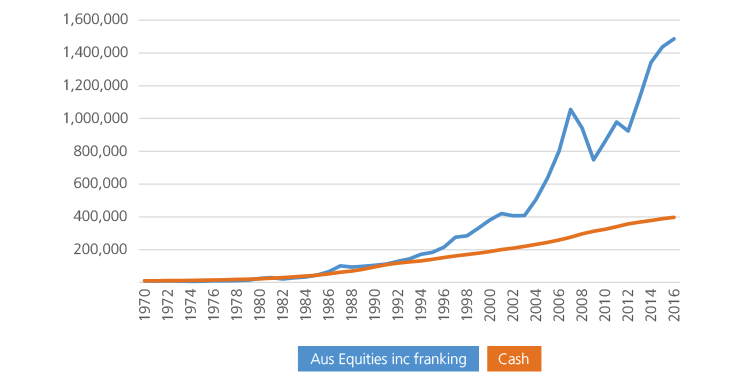

Cumulative Return on $10,000

Source: Vanguard Investments Australia, Athena IOC

The second chart above shows the cumulative returns of $10,000 invested in Australian equities and cash over the same 46-year period. Coincidentally 46 years is exactly the time a fund member entering the work force at the age of 21 and retiring at 67 would have funds invested in the accumulation phase of superannuation.

Clearly investing in the lower volatility asset class over the long term is by far the riskier option if the risk is “running out of money in retirement”. Some would argue that the member would have a far greater amount invested at the end of the 46-year period than at the beginning and the “risks” are greater at that point in time. Again, this view looks only at short term volatility and not at the real risk.

History tells us over this 46-year period that we should expect negative returns for Australian equities approximately five times in every 20 years. It follows that the chance of a positive year is three times greater than the chance of a negative year. If money is moved out of growth assets when the member’s balance is approaching its highest, the member is likely to forego a significant increase in their final balance at the end of their accumulation phase.

It should be further noted that the end of the accumulation phase is not a magical point in time where the superannuation balance suddenly dematerialises, is converted to an annuity or is stuffed under a mattress. From the point of retirement the balance is usually drawn down over a period of around a quarter of a century in very small increments. Even in draw down phase the bulk of a member’s money remains invested in the market over a very long term.

How to measure risk

In order to develop a model for practical and meaningful measurement of the real risk facing the superannuation fund member in retirement, assumptions need to be made about key data elements:

- The member’s balance at commencement of pension phase. In the following analysis the assumption has been based on the ASFA Retirement Standard for a comfortable lifestyle for a couple

- Annual withdrawals to meet living expenses. Again, from ASFA’s Retirement Standard for a comfortable lifestyle for a couple

- Investment market returns. Actual market returns for the 46-fiscal year period from July 1970 to June 2016 have been adopted

- Inflation per the Australian Bureau of Statistics web site over the same 46-year period.

Assumptions

- Balance at commencement of pension = $640,000 at 1 July

- Annual withdrawal = $59,808 at mid-year, indexed annually with CPI

- Australian equities annual earnings = ASX All Ords total return index grossed up for (conservatively) estimated franking credits

- Cash annual earnings = Bloomberg Australian Bank Bill Index

- Period covered = 1970 – 2016 (46 years)

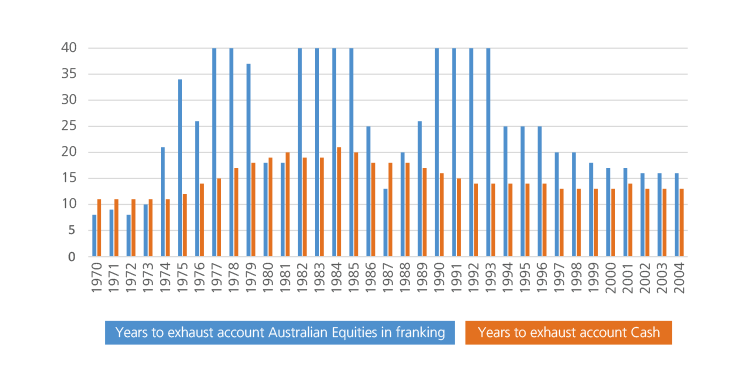

The next chart shows the estimated years to exhaust the member’s account if we assume a commencement of pension drawdown form 1 July 1970, 1971, 1972 and so on, up to 2004.

Estimated Years to Exhaust Account

Source: Athena IOC

The chart shows that for a member who retires in market conditions prevailing from 1970 it would take around 11 years to exhaust their account if they were fully invested in cash and around eight years if fully invested in Australian equities. For a member commencing retirement in market conditions prevailing in 1975, cash is estimated to last for 12 years and Australian equities for 34 years.

Overall it is estimated that Australian equities would outlast cash 80 per cent of the time and of course cash would outlast Australian equities 20 per cent of the time.

If risk is defined as “running out of money during retirement”, clearly Australian Equities is far less risky even though it is undoubtedly the more volatile asset class.

Alternative risk measures compared

Traditional risk measures

| Option | Std Deviation | Max Drawdown (%) | No of Negative Years in 20 |

|---|---|---|---|

| Australian Equities | 12.0 | 45.0 | 6 |

| Cash | 1.0 | 5.0 | 0 |

| Conservative | 3.1 | 10.6 | 1 |

| Balanced | 6.3 | 24.2 | 3 |

| Aggressive | 8.8 | 34.7 | 4 |

| CIPR | 3 | 11 | 2 |

| Etc | x | x | x |

The above table provides information about the relative volatility of different investment options. But what meaningful information does it convey to a member or an adviser at the point of rolling into pension phase? There is nothing in this information that provides any guidance as to whether the member’s account will last through their retirement – that is, nothing to provide any information as to the relative real risk of the options. The risk of running out of money in retirement.

RRM (Ringrose Risk Measure)

In this example a new risk measure entitled the ‘Ringrose Risk Measure’ is introduced. Assuming a starting balance of $640,000, annual withdrawals of $59,808 and actual historical market returns and CPI movements.

| Probability of Maintaining Positive Account Balance (%) | |||

|---|---|---|---|

| Option | Over 7 Years | Over 7 Years | Over 25 Years |

| Australian Equities | 100 | 84 | 53 |

| Cash | 100 | 41 | 0 |

| Conservative | x | x | x |

| Balanced | x | x | x |

| Aggressive | x | x | x |

| CIPR | x | x | x |

| Etc | x | x | x |

It could be argued that the above table provides significant information to assist the member in choosing an appropriate investment option for their retirement. It addresses the key question “what is the risk of running out of money in retirement?” This or a similar table could be included in its generic form in any PDS.

The above information is capable of measurement for any proprietary comprehensive income product for retirement (CIPR) or member investment choice option.

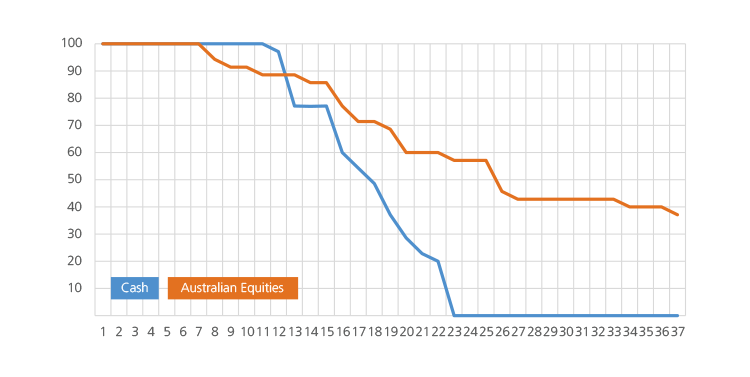

The table above can be further enhanced to produce information in chart form providing more detailed and member specific information. Such a chart is shown below.

Probability of Maintaining a Positive Balance

Source: Athena IOC

In this example we can see that, given the same assumptions as noted in the table above, an investment in Cash has a 100 per cent probability of lasting for 11 years whilst an investment in Australian Equities provides only an 88 per cent chance of lasting the same length of time.

Conversely, an investment in Cash provides around a 25 per cent probability of lasting 20 years against a 60 per cent probability for Australian Equities. Interestingly, cash provides a 0 per cent probability of lasting 25 years compared with a 55 per cent chance for Australian Equities.

This chart can be made interactive for financial planners and members to test various scenarios of start balances and annual drawdowns. It could of course also incorporate any CIPR or investment choice options available to the member. Such information would enable the member to make an informed choice re their preferred risk mitigation strategy based on their expectations of longevity. Such a choice could be revisited on an annual or other periodic basis to assess the optimum strategy going forward. For example, choosing a less volatile option if the prevailing current account balance could support the required withdrawals at the desired level of risk.

Concluding thoughts

The relative risk of different asset classes or investment choice options can vary dramatically over different time horizons. It appears that this fact has not been fully appreciated by all superannuation funds and certainly not by their members. Although one major fund’s PDS describes various levels of risk for different time horizons, this appears to be an exception and not the rule.

The analysis in this article poses the following questions which could merit further research:

- Does a less volatile investment strategy provide a misleading illusion of safety and lower real risk to superannuation fund members?

- Can that illusion of safety/lower risk result in (potentially significantly) less money in retirement? (that is, higher risk!)

- Are many in the industry confused about the difference between risk and market volatility in the context of superannuation funds’ long horizon investment?

- Are superannuation funds really acting in the best interests of members by:

- Describing less volatile options as less ‘risky’?

- Moving members into less volatile asset classes as they approach retirement?

It’s all about the definition of ‘risk’

This article asserts that risk to a member of a superannuation fund is not market volatility. Risk is “running out of money in retirement”. Paradoxically by adopting an inappropriate definition of risk, superannuation funds are promoting less volatile investment strategies as reducing risk when in fact they are increasing risk! This should be of great concern to the superannuation industry.

DISCLAIMER

Whilst the numbers used in this article are indicative only, the overarching message remains consistent. This article is not intended to constitute advice. Readers should seek personalised advice from a suitably qualified source.