The Federal Government has proposed reducing the concession paid on earnings in superannuation accounts holding more than $3 million dollars.

HOW TAX ON SUPERANNUATION INVESTMEN EARNINGS IS CALCULATED

Current tax treatment

Currently superannuation fund investment earnings (other than investment earnings associated with retirement accounts) are taxed at a headline rate of 15 per cent. However, that part of investment earnings attributable to capital gains in regard to assets held more than 12 months receives a one-third discount, effectively reducing the tax rate to 10 per cent on realised capital gains. There also will be imputation credits connected with share dividends that can be used to offset tax liabilities and which are refundable if there is no tax liability.

Investment returns associated with retirement accounts are tax-free. There is a limit to the amount an individual can place in the retirement accounts, with this called the Transfer Balance Cap. This cap is indexed and is currently at $2 million. Those who have set up a retirement account in the past may have had a lower Transfer Balance Cap. The amount each individual can have in a retirement account will depend on their initial Transfer Balance Cap and subsequent investment earnings and withdrawals. Current balances in regard to which investment earnings are tax free will vary from individual to individual. Balances supporting tax free investment returns often will be below $2 million but it is possible to have a higher balance, even exceeding $10 million, if investment returns (including capital gains) have been strong.

Currently for retirees with large balances a proportion of their total balance will have investment earnings tax free with the remainder having the same tax treatment applicable to pre-retirement balances. The proportion will depend on individual circumstances rather than being a simple calculation based on the total amount of superannuation a person has.

Proposed Division 296 tax

The proposed tax on imputed investment earnings associated with the proportion of earnings attributed to balances above $3 million also employs a headline rate of 15 per cent, but as shown by the examples below a number of adjustments are made in calculating the tax liability. The 15 per cent Division 296 tax rate cannot be simply added to the current headline rate to come up with a total effective tax rate on investment earnings.

While current taxation of superannuation investment earnings uses traditional measures of taxable income, the taxable earnings under Div 296 are found by deducting the total super balance accounts held by an individual at the start of the year from the balance at the end of the year, adding some outgoings such as pension payments, and subtracting some items that increased the balance, like super contributions.

Because the tax is calculated on valuations at a point in time, it requires at least annual market valuations of assets to be undertaken. Both APRA regulated funds and SMSFs are already required to undertake at least annual market valuations of assets held.

There also are around one million Australians who have an account in a defined benefit fund. Defined benefit superannuation funds do not have account balances or investment earnings that are attributable to individual fund members. Actuarial calculations are needed to calculate what the value of a defined benefit fund member’s interest in their superannuation. The Government is proposing that the valuation factors used for Family Law splitting of benefit purposes should be used for the Division 296 tax calculation. Only a relatively small proportion of defined benefit fund members will have benefit entitlements that have an actuarial value of over $3 million.

Members of defined benefit funds also generally do not have access to their superannuation until they retire. These differences from the more common accumulation accounts in superannuation generally mean the Div 296 tax would be calculated each year, but only paid when the member retires.

The worked examples below show how the tax is calculated for a range of different superannuation account holders. The examples below are for illustration purposes only and based on current information about the proposed tax as at 5 June 2025.

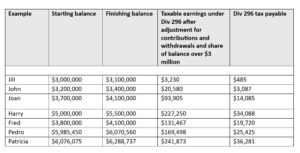

Joan, a retiree with account-based pensions

In the 2025–26 income year Joan received benefit payments of $250,000 combined from her two pension accounts and made a $300,000 downsizer contribution. On 30 June 2025 Joan’s Total Superannuation Balance (TSB) was $3.7 million and $4.1 million on 30 June 2026.

Joan’s adjusted TSB at the end of the year is calculated to be $4.05 million by adding her total withdrawals of $250,000 and deducting her total contributions of $300,000 from her 2025–26 TSB of $4.1 million. Her superannuation earnings for the year are $350,000 (the difference between $4.05 million and $3.7 million).

The percentage of taxable earnings over $3 million is calculated by subtracting $3 million from $4.1 million and then dividing it by $4.1 million, resulting in a percentage of earnings attributable to the balance over $3 million of 26.83 per cent.

The Division 296 tax amount is calculated by first multiplying the superannuation earnings of $350,000 by 26.83 per cent, which is $93,905. That amount is then multiplied by the 15 per cent tax rate, leading to a Division 296 tax amount of $14,085.75. This is a relatively small proportion – approximately 4% – of the overall superannuation earnings of $350,000.

Jill, not currently working, aged 55

On 30 June 2025 Jill’s Total Superannuation Balance (TSB) was $3.0 million and $3.1 million on 30 June 2026.

Her superannuation earnings for the year are $100,000 (the difference between $3.1 million and $3.0 million).

The percentage of taxable earnings over $3 million is calculated by subtracting $3 million from $3.1 million and then dividing it by $3.1 million, resulting in a percentage of earnings attributable to the balance over $3 million of 3.23 per cent.

The Division 296 tax amount is calculated by first multiplying the superannuation earnings of $100,000 by 3.236 per cent, which is $3,230. That amount is then multiplied by the 15 per cent tax rate, leading to a Division 296 tax amount of $485.

John, an employee who has not retired

In the 2025–26 income year John had total employer contributions totalling $25,000 after deduction of the 15 per cent contribution tax. On 30 June 2025 John’s Total Superannuation Balance (TSB) was $3.2 million and $3.4 million on 30 June 2026.

John’s adjusted TSB at the end of the year is calculated to be $3.375 million by deducting his total contributions of $25,000 from his 30 June 2026 TSB of $3.4 million. His superannuation earnings for the year are $175,000 (the difference between $3.375 million and $3.2 million).

The percentage of taxable earnings over $3 million is calculated by subtracting $3 million from $3.4 million and then dividing it by $3.4 million, resulting in a percentage of earnings attributable to the balance over $3 million of 11.76 per cent.

The Division 296 tax amount is calculated by first multiplying the superannuation earnings of $175,000 by 11.76 per cent, which is $20,580. That amount is then multiplied by the 15 per cent tax rate, leading to a Division 296 tax amount of $3,087. This is a relatively small proportion – less than 2% – of the overall superannuation earnings of $175,000.

Harry, self employed and not retired

On 30 June 2025 Harry’s Total Superannuation Balance (TSB) was $5 million and $5.5 million on 30 June 2026.

Harry made no contributions and had no withdrawals from his super, so the superannuation earnings for the purpose of the tax are $500,000, the difference between the two figures.

The percentage of taxable earnings over $3 million is calculated by subtracting $3 million from $5.5 million and then dividing it by $5.5 million, resulting in a percentage of earnings attributable to the balance over $3 million of 45.45 per cent.

The Division 296 tax amount is calculated by first multiplying the superannuation earnings of $500,000 by 45.45 per cent, which is $227,250. That amount is then multiplied by the 15 per cent tax rate, leading to a Division 296 tax amount of $34,088.

Fred the retired farmer

Fred has retired from farming. His children continue the farming business, paying rent to the Self-Managed Super Fund (SMSF) which holds the property as an investment asset.

Fred’s account in the SMSF has an investment portfolio represented by the $3 million value of the farm, together with shares and bank deposits. His total superannuation balance as at 30 June 2025 is $3.8 million. The fund receives rent in 2025–26 at a yield of 4 per cent on the opening value of the land, which equates to $120,000. The SMSF is required to charge a commercial rent for the farming land. Rent is a set amount and does not vary with the profitability (up or down) of the farming business.

Interest and dividends amount to $60,000 a year. Fred draws down at the minimum required rate for his age (70), so his benefit payment is $190,000 in 2025–26. Even in the absence of any Division 296 tax the fund needs to have access to cash to pay the minimum required drawdown.

At 30 June 2026 the value of his interest in the farm has increased by 10 per cent to $3.3 million. The total value of his interest in the SMSF is $4.1 million.

Fred’s adjusted TSB at the end of the year is calculated to be $4.29 million by adding his total withdrawals of $190,000. His superannuation earnings for the year are $490,000 (the difference between $4.29 million and $3.8 million).

The percentage of taxable earnings over $3 million is calculated by subtracting $3 million from $4.1 million and then dividing it by $4.1 million, resulting in a percentage of earnings attributable to the balance over $3 million of 26.83 per cent.

The Division 296 tax amount is calculated by first multiplying the superannuation earnings of $490,000 by 26.83 per cent, which is $131,467. That amount is then multiplied by the 15 per cent tax rate, leading to a Division 296 tax amount of $19,720. This is approximately 4% of the overall superannuation earnings of $490,000 and around 10 per cent of the otherwise tax-free payment he received from superannuation.

Pedro, retired male MP

Pedro retired from Parliament in May 2025 after many years of service, including as a Minister and Shadow Minister. Due to his date of entry to Parliament he qualifies for a defined benefit pension which he started to receive from May 2025. He has informed the fund trustee that he has a spouse. He is aged 55 as at 30 June 2025.

In the 2025–26 income year Pedro received benefit payments of $250,000.

The trustee of the fund has used the Family Law valuation method to determine a Total Superannuation Balance (TSB) of $5,985,450 on 30 June 2025 and a closing balance of $6,070,560 as at 30 June 2026. The closing balance reflects a lower valuation factor due to the member being one year older but there is also an increase in the benefit paid, which for the purpose of this illustration is indexed by growth in average earnings of 3.5 per cent.

Pedro’s adjusted TSB at the end of the year is calculated to be $6,320,560 by adding his total withdrawals of $250,000. His calculated superannuation earnings for the year are $335,110 (the difference between $6,320,560 and $5,985,450).

The percentage of taxable earnings over $3 million is calculated by subtracting $3 million from $6,070,560 and then dividing it by $6,070,560, resulting in a percentage of earnings attributable to the balance over $3 million of 50.58 per cent.

The Division 296 tax amount is calculated by first multiplying the superannuation earnings of $335,110 by 50.58 per cent, which is $169,498. That amount is then multiplied by the 15 per cent tax rate, leading to a Division 296 tax amount of $25,425 from $335,110 in earnings.

Patricia, retired female MP

Patricia also retired from Parliament in May 2025 after many years of service, including as a Minister, Shadow Minister and Committee Chair. Due to her date of entry to Parliament she qualifies for a defined benefit pension which she started to receive from May 2025. She has informed the fund trustee that she has a same-sex spouse. She is aged 55 at 30 June 2025.In the 2025–26 income year Patricia received benefit payments of $250,000.

The trustee of the fund has used the Family Law valuation method to determine a Total Superannuation Balance (TSB) of $6,076,075 on 30 June 2025 and a closing balance of $6,288,737 as at 30 June 2026. The closing balance reflects both a lower valuation factor due to the member being one year older and also an increase in the benefit paid (to $258,750), which for the purpose of this illustration is indexed by growth in average earnings of 3.5 per cent.

The Family Law valuations use gender-based factors, reflecting longer life expectancy for women. A higher valuation also applies when there is a spouse, because of the reversionary pension paid on the death of the primary recipient. The valuation factors assume a spouse is of the opposite gender. It is also not clear whether the factors apply to a person based on their gender at birth or the gender they currently identify with.

Patricia’s adjusted TSB at the end of the year is calculated to be $6,538,737 by adding her total withdrawals of $250,000 to the closing balance. Her calculated superannuation earnings for the year are $462,562 (the difference between $6,538,737 and $6,076,075).

The percentage of taxable earnings over $3 million is calculated by subtracting $3 million from $6,288,737 and then dividing it by $6,288,737, resulting in a percentage of earnings attributable to the balance over $3 million of 52.29 per cent.

The Division 296 tax amount is calculated by first multiplying the superannuation earnings of $462,562 by 52.29 per cent, which is $241,873. That amount is then multiplied by the 15 per cent tax rate, leading to a Division 296 tax amount of $36,281 – around 14 per cent of the pension received.

The Division 296 tax payable by Patricia is about 45 per cent more than the tax payable by Pedro, even though they receive the same pension payment. This is due to the use of gender-based valuation factors. The calculated investment earnings are higher and a greater amount of the account balance is over $3 million. In submissions on the valuation methods ASFA has advocated for the same valuation factors to apply to males and females for both the primary and reversionary beneficiaries.

For further information, please contact:

ASFA Media Manager Richard Garfield, 0451 949 300.

About the Association of Superannuation Funds of Australia (ASFA)

ASFA, the voice of super, has been operating since 1962 and is the peak policy, research and advocacy body for Australia’s superannuation industry. ASFA represents the APRA regulated superannuation industry with over 100 organisations as members from corporate, industry, retail and public sector funds, and service providers. We develop policy positions through collaboration with our diverse membership base and use our deep technical expertise and research capabilities to assist in advancing outcomes for Australians.

We unite the superannuation community, supporting our members with research, advocacy, education and collaboration to help Australians enjoy a dignified retirement. We promote effective practice and advocate for efficiency, sustainability and trust in our world-class retirement income system.